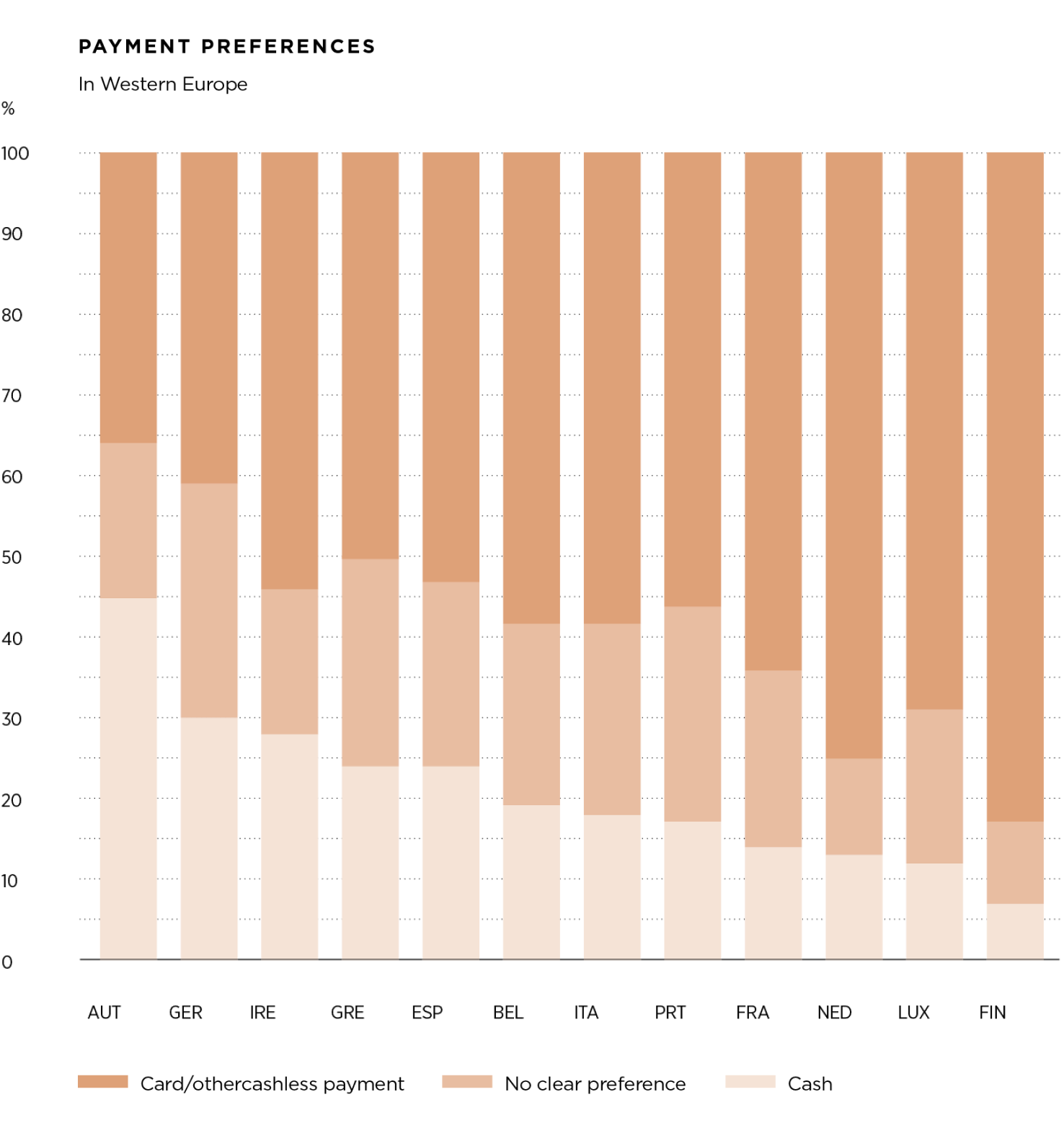

Currently, more than half of all daily transactions in Europe are made with cash. However, a study from the ECB shows that while cash is still the most frequently used means of payment, its use is rapidly declining and will be at under 50% in the next few years. Our research team looks at the future of finance and what this big shift in consumer behaviour means for investors.

Globally, cash usage has lost nearly 20% in share of global payments over the past five years, during which time the growth rate of electronic transactions has nearly tripled. By 2027, cash-heavy developing economies are likely to make further significant shifts towards cashless instant payments. This will bring the transaction share of electronic payments to nearly two and a half to three times greater than in 2022.

| CASHLESS PAYMENTS IN E-COMMERCE

One of the main reasons for the rapid growth in digital payments during the past few years has been the rise of e-commerce. The COVID-19 pandemic boosted e-commerce revenues across most countries. At the peak of the pandemic, even more was purchased online, which has pushed parts of the e-commerce industry into a post-pandemic hangover.

The structural growth of e-commerce is set to continue, expanding into underpenetrated geographies, such as Latin America/ Southern and Eastern Europe, and into new segments, such as food or pharmaceuticals. This growth is driven by the benefits e-commerce brings to both sides of the transaction. For the retailer, it offers a bigger reach and a broader customer base, while reducing operating costs. It also improves communication with customers, allowing for better targeting and the ability to offer personalised goods.

For the consumer, e-commerce saves time, offers a hassle-free shopping experience and increases the choice of products and services. It also provides the opportunity to shop outside of core business hours and local demographic, to make informed choices, and obtain attractive prices.

The structural growth of e-commerce bodes well for card payments as well. More than 50% of consumers prefer to use debit or credit cards for online payments, according to the JP Morgan Online Checkout Survey. Add in mobile wallets, which are most often linked to credit cards, and the dominance of cards as the preferred means of payment becomes even bigger. As such, we see payment network providers and related companies as the main beneficiaries of the structural growth of e-commerce.

| NEW FORMS OF DIGITAL PAYMENTS

Despite providing such a basic and unspectacular service, the payment industry is constantly innovating, offering more convenient and simpler solutions. Looking ahead the focus will be on faster payment speeds, so-called ‘real-time payments’, which are state-of-the-art in some parts of the world and buy now pay later programs.

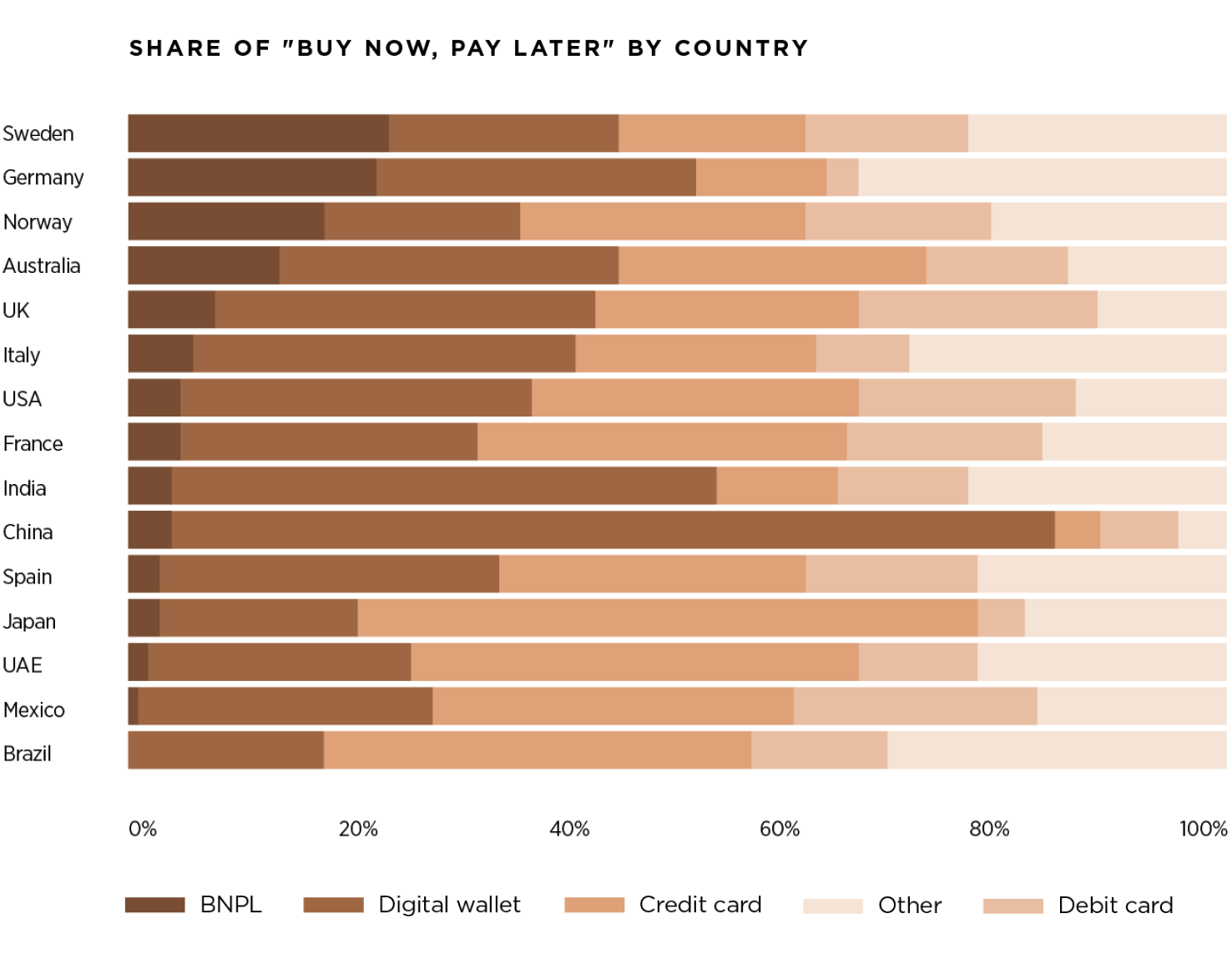

Buy now, pay later

‘Buy Now, Pay Later’ (BNPL) is an innovation offering consumers the flexibility to pay for purchases at a later point in time or in instalments over a period of time. Depending on the options offered, ‘Buy now, pay later’ providers generate income either directly from consumers via interest or fee payments or indirectly from merchants via a discount rate, ranging from 2% to 8%.

According to studies, consumers using BNPL are not only up to three times more likely to complete a purchase after browsing, but also typically shop more. BNPL allows a transaction to be split into smaller, interest- free instalments that can be repaid over time. The typical structure divides a USD 50 to USD 1,000 purchase into four equal instalments, starting with a down payment due at checkout, and the next three payments due at two-week intervals over six weeks.

Real-time payments

Today’s payment system is both sophisticated and safe, but in some instances lacks speed. Bank transfers and credit card payments sometimes still take between two to three days, and with today’s degree of digitalisation and processing power, real-time payments (RTP) should be the norm, not the exception.

The introduction of real-time payments is set to overcome this as payments will be initiated, cleared, and settled within seconds, at any time of the day or week, holidays and weekends included. This improves transparency and confidence in payments, thus helping consumers, banks, and businesses manage their money.

he ECB’s TARGET Instant Payment Settlement (TIPS) service was launched in 2018, enabling real-time payments settlement 24 hours a day, 365 days a year, including weekends and holidays. In the United States, the Federal Reserve began developing its FedNow service in 2019, which went live this summer. Furthermore, real-time payments in the United States are facilitated through the Clearing House’s RTP network, which was established in 2017. Globally, real-time payments systems are available in more than 70 countries, processing a total of 195 billion transactions in 2022, up 63% year-on-year.

"According to studies, consumers using BNPL are not only up to three times more likely to complete a purchase after browsing, but also typically shop more. BNPL allows a transaction to be split into smaller, interest- free instalments that can be repaid over time"

| KEY TAKE-AWAYS

➊ Digital payments are the soundest structural growth story in the financial services industry, reflecting the rise of e-commerce and the preference for cashless payments.

➋ Already tripled in the last five years, the use of digital payments is set to triple again in the next five years.

➌ Looking ahead the focus will be on faster payment speeds and so-called ‘real-time payments'.

| WHAT DOES THIS MEAN FOR INVESTORS?

Digital payments are the soundest structural growth story in the financial services industry, reflecting the rise of e-commerce, growing international travel, and the preference for cashless payments. We are observing an evolutionary environment rather than a revolutionary one in the financial industry and this is unlikely to change in the foreseeable future providing unique opportunities for investors.

Julius Baer

International wealth management group, based on a solid Swiss heritage. Special thanks to Carsten Menke & Nikolaus Werner.

juliusbaer.com