Despite three years of uncertainty and market volatility (2020-2022) given Covid-19, oil prices swings, inflationary pressures, and the Russia-Ukraine war, 2023 and 2024 have been turnaround years. During 2023-2024, the economy experienced a supply-side economic effect which led to an increase in production of goods and services, expansion of employment and decrease in inflation.

For end of 2025, the S&P 500 base case is 6,600 and bull case 6,800 points. Our goldilocks soft-landing base case scenario remains intact for 2025 as inflation continues on a sustainable path to 2% target, financial conditions are easing and the US economy is expected to grow at a moderate pace. However, navigating this path requires a cautious investment approach as macroeconomic imbalances, two ongoing wars, trade protectionism and rising populism are building up tail risks. In the current environment, the forward paths of inflation, employment, economic growth, interest rates, earnings, valuations, and geopolitical outcomes are difficult to predict.

The US, the world’s largest economy, was able to avoid a recession in 2023 as the GDP grew 2.9% and is expected to grow 2.8% in 2024 and 2.3% in 2025 according to Goldman Sachs. Consumer spending in the US continues to be robust, business investment remains relatively strong, inflation is declining but remains slightly above the FED 2.0% objective, and labor market continues to expand at a slower pace with the unemployment rate steadily rising, currently at 4.4%. During 2023, the US labor market added 2.7 million jobs and average hourly earnings grew at a moderate pace. However, during 2024 labor supply growth is running around 200,000 average jobs per month adding 1.8 million jobs year to date.

The 11 FED rate hikes between March 2022 and July 2023 reached a peak rate in the range of 5.25% - 5.50% have put the US economy on track for a goldilocks scenario. For the first time in four years, the FED cut short-term rates by 50 basis points (bps) at the September FOMC meeting, in light of the good inflation news and the risk of further labor market softening. The rationale for the bold cut was the shift in focus from inflation risks to employment risks and the FED determination not to fall behind the curve in the easing cycle. The annual Consumer Price Index (CPI) in the US reached 7.0% at the end of 2021, 6.5% at the end of 2022, 3.4% at the end of 2023 and is expected to reach 2.3% in 2024 and 2.0% in 2025, according to the US Bureau of Labor Statistics & Goldman Sachs.

Market participants are expecting 1 more cut in 2024 and 4 cuts in 2025 forecasting the terminal federal funds target rate to range between 4.25% and 4.5% at the end of 2024 and 3.0% and 3.25% at the end of 2025.

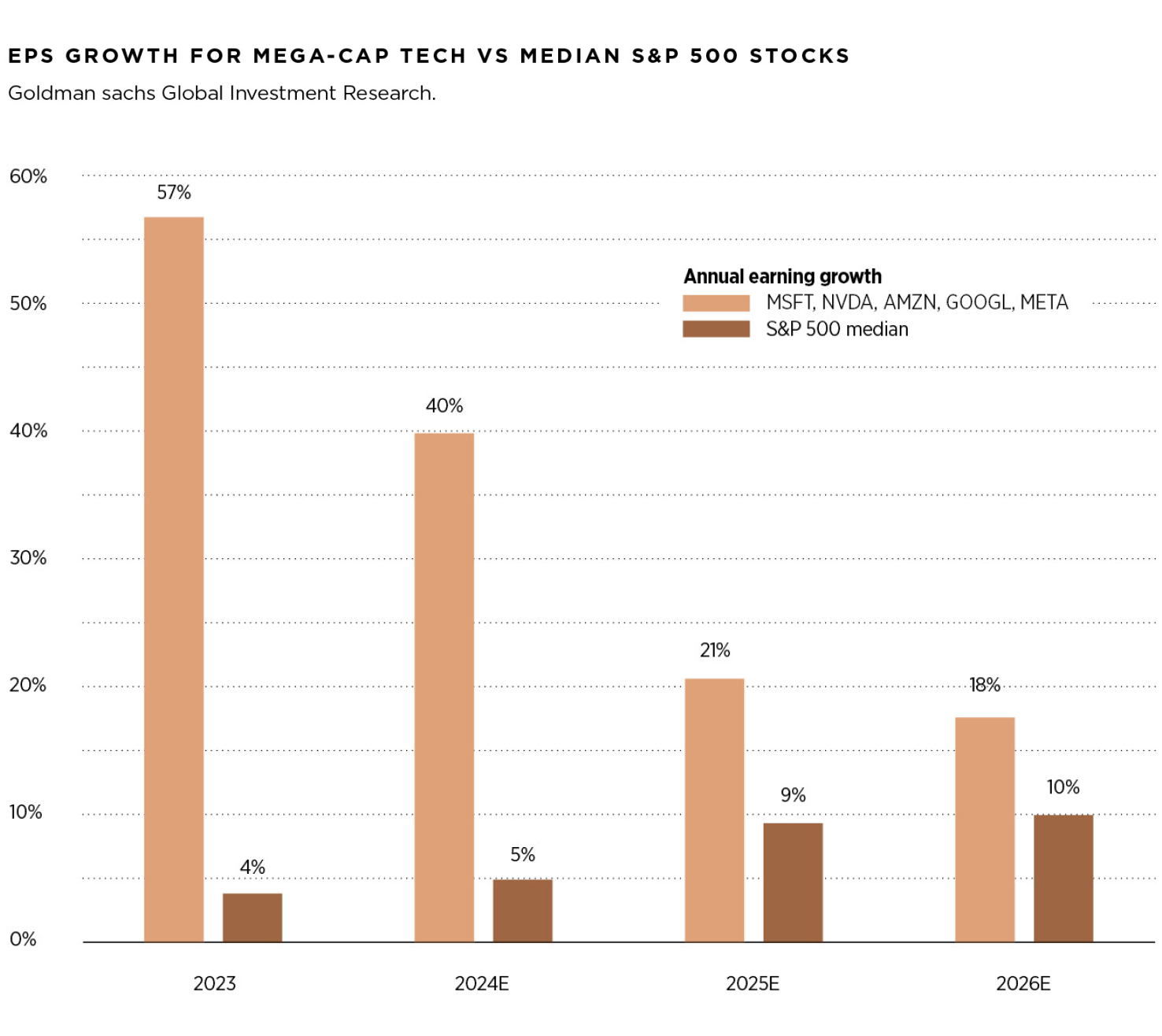

On October 12, 2022 the index reached a low of 3,577 trading at a P/E of 15x. The 10-year US Treasury Note hit a 16-year high of 4.99% in October 19, 2023. The three major US indexes S&P 500, NASDAQ & RUSSELL confirmed a bear market on June 13, 2022 and the DOW confirmed a bear market until September 30, 2022, often a bear market precedes a recession. However, after US’s main indexes entered into bear market territory in 2022, most US stocks, in particular the so-called “Magnificent 7” have rallied in 2023 and 2024 as signs of easing inflation, a more accommodative monetary policy stand, earnings growth and technological transformation. Strong performance by MSFT, NVDA, AAPL, GOOG, AMZN and META has contributed around 44% of the index return. On October 18, 2024, the S&P 500 index reached a new all-time high of 5,865 posting a total return of more than 60% from trough-to-peak.

In general, long-term equity returns are driven by the earnings growth of the asset and the change in valuation. In 2023, the S&P 500 EPS closed at USD $223 and is expected to grow 8% to USD $241 in 2024 and 12% to USD $270 in 2025.

Since the end of the Global Financial Crisis (GFC), technology, in particular, large language models and generative AI, have been the most important driver of returns for the US and global equity markets. Even during periods of economic uncertainty, companies continue to invest in technology. The outperformance of tech stocks in recent years has far outstripped other major sectors as a result of stronger fundamentals rather than irrational exuberance. Compared with the peak of the Tech Bubble, the 10 largest stocks today trade at elevated valuations, 25x P/E in 2024 but not at record multiples, 43x P/E in 2000. However, this outperformance has also lifted US equity market concentration to the highest level in decades. The 10 largest stocks now account for 33% of S&P 500 market cap, well above the 27% share reached at the peak of the Tech Bubble in 2000.

As of Oct 22, 2024, the S&P 500 index is up 23% trading at a P/E of 25x. The NASDAQ is 24%, RUSSELL 3000 is 21%, the DOW is 14% and the 10-year US Treasury Note yielded 4.2%.

According to Goldman Sachs the outlook for global growth will slow from 3.0% in 2022 to 2.8% in 2023, 2.7% in 2024 and 2.8% in 2025, well below the 3.8% historic average of the past two decades. Global inflation is forecast to decline, from 6.5% in 2022 to 4.3% in 2023, 3.2% in 2024 and 2.7% in 2025. The growth rate forecast for China, the world’s second-largest economy, is expected to reach 5.2% in 2023, 4.9% in 2024 and 4.7% in 2025. China’s economy is facing growing headwinds because of declines in real estate investment, housing prices, weak consumer sentiment and ongoing demographic deterioration. However, the 2024 GDP growth and fiscal targets laid out by top China officials reiterated policymakers continued focus on bolstering economic growth during 2024. The Euro Area is expected to slow from 3.4% in 2022 to 0.5% in 2023, yet the growth rate forecast for 2024 is 0.7% and 1.1% in 2025, as a result is likely to avoid a recession.

The outlook for 2025 and beyond, looks challenging and uncertain. Geopolitical risk posed by two ongoing wars, oil supply disruptions and trade conflict have inevitable knock-on effects on the economy. While the US economy remains relatively strong, the political system is currently more dysfunctional than any other advanced industrial democracy. As the US presidential election approaches between former President Trump and Vice President Harris, it is expected a very close match as they present very different worldviews and policy agenda when it comes to the economy, trade, tariffs, taxes, regulation, immigration, national defense and border security.

Global trade boomed in the 1990s and early 2000s as the World Trade Organization (WTO) was created in 1995 and has helped facilitated multilateral trade agreements and dispute settlement mechanisms. However, as a result of rising geopolitical tensions, trade has stabilized after a level of “hyper globalization” between 1986 and 2008. In particular, trade openness slowed following the global financial crisis (GFC) a trend that may be pointing to a possible reversal of globalization. However, China share of global trade continues to increase rapidly after it joined the World Trade Organization (WTO) in 2001.

The US Federal government debt reached USD $35 trillion dollars at the end of 2024. The debt-to-GDP ratio has increased from a pre-GFC low of 35% in 2007 to 123% in 2024 and is likely to increase over the next decade. This debt trajectory is not sustainable and is uncertain where the tipping point might be. The US debt limit crisis in 2011 ended with a compromise that averted default but prompted downgrades by S&P Global Ratings as it stripped the US from its top score and sent the S&P 500 down 17%. In August 2023, Fitch Ratings downgrade the US debt to AA+ from AAA and in November 2023, Moody’s lowered the US sovereign outlook to negative from stable while affirming the rating of AAA, the highest investment-grade notch. US policy-making has become less stable, less effective and less predictable as intensifying polarization and dysfunction in the decision-making process is evident among US elected officials.

The US government runs persistent budget deficits as it spends more than it collects in revenue. According to the US Treasury, fiscal deficit is expected to reach USD $1.9 trillion at the end of 2024 around 6.5% of GDP, almost double the USD $984 billon level in 2019. Net interest payments due on federal debt are likely to exceed USD $1 trillion per year, around 3.5% of GDP. The tax and spending policies implemented by the upcoming administration will have significant effects on the size of future budget deficits, fiscal strength and credit profile of the US sovereign debt. For example, extending or allowing the 2017 Tax cuts and Jobs Act to expire and the ever-growing litany of tax breaks, incentives, special zones, tariffs and corporate tax reductions promised during the presidential campaign by both Donald Trump and Kamala Harris will have an important impact in the US budget. The next US president is unlikely to have control over Congress, as a result, campaign promises do not often translate into legislative action. However, if for some reason the tax proposals promised during the campaign are enacted they would likely shift the economic outlook and the performance of markets. Despite all these challenges, we expect the US government will ultimately maintain its fiscal prudence, resolve any debt limit disputes and continue to pay its obligations on time and in full.

“In August 2023, Fitch Ratings downgrade the US debt to AA+ from AAA and in November 2023, Moody’s lowered the US sovereign outlook to negative from stable while affirming the rating of AAA, the highest investment-grade notch. US policy-making has become less stable, less effective and less predictable as intensifying polarization”

During the summer of 2024, oil prices fluctuated back and forth in the range of USD $75-90 per barrel as market focus on geopolitical risks to oil supply and concerns about the health of consumption in the West and China. WTI is trading at USD $72 per barrel, Brent at USD $76 per barrel and natural gas at USD $2.30 per million of BTU. According to Goldman Sachs estimates, Brent prices are expected to range USD $70-$85 per barrel in 2025 as a result of stronger Iran and Russia oil production and non-OPEC supply growth. In addition, oil demand in China is slowing as a result of structural road fuel switching toward power (EVs), natural gas (LNG trucks), and on petrochemical demand weakness. However, Russia output cuts, Iran supply reductions, Red Sea disruptions, OPEC production postponed and international travel recovery cannot be ruled out. OPEC formation occurred in 1960 by five founding members: Iran, Iraq, Kuwait, Saudi Arabia and Venezuela at a time of transition in the international economic and political landscape. While oil markets are not currently pricing a worst-case scenario of the Middle East crisis as it did in the 1970s (Arab-Israeli war/Oil embargo), 1980s (Iran-Iraq war) and 1990s (invasion of Kuwait), the tail risk of a very large oil price spikes remains as a result of rising geopolitical, oil supply disruptions and the escalation of two ongoing wars.

The dollar, gold and Treasuries will likely gain from further safe-haven flows in more adverse escalation scenarios in the Middle East. The Basel Committee on Banking Supervision was set up in 1974 by central banking governors of the Group of Ten countries in order to maintain oversight of global banking standards and higher levels of capital adequacy. The new Basel III Accords, implemented across various regions since 2021, treat gold held in vaults as a zero-risk asset and classifies it as a Tier 1 Asset, a status previously reserved for cash. These rules mean banks must hold more high-quality assets like gold to safeguard against financial crisis. This regulatory shift is expected to influence gold demand significantly, driving prices up and reaffirming gold’s role a secure and stable investment. Gold price reach a record high of USD$ 2,761 per ounce on October 22, 2024 and according to some market participants it is expected to reach USD $3,000 per ounce for early 2025.

“On November 8, 2021, Bitcoin reached a record high of USD $67,000 and the market value of cryptoassests peaked at around USD $3 tillion. However, the bubble burst in early 2022, tigerred by the collapse of the then third largest stablecoin TerraUSD. In November 2022, the bankruptcy of FTX, one of the world’s largest crypto exchange platforms sent shockwaves through the ecosystem”

Ever since since the GFC (2007-2009) and even more pertinent in the face of the Covid-19 crisis (2020-2022), goverments and central banks have lanunched vast stimulus and rescue programs to bailout financial institutions and the economy. In 2009 someone identified as Satoshi Nakamoto succesfuly launched Bitcoin, a peer-to-peer payment network that operates without intermediaries, consensus mechanisms, smart contract capability and no need for bailouts. Since then, its underlying blockchain technology has inspired an entire new ecosystem of plataforms and protocols with a wide range of applications. On November 8, 2021, Bitcoin reached a record high of USD $67,000 and the market value of cryptoassests peaked at around USD $3 tillion. However, the bubble burst in early 2022, tigerred by the collapse of the then third largest stablecoin TerraUSD. In November 2022, the bankruptcy of FTX, one of the world’s largest crypto exchange platforms sent shockwaves through the ecosystem. However, the FTX blowup has not destroyed all faith in the industry, in particular Bitcoin. On March 13, 2024, Bitcoin reached a new all-time high of USD $73,157 and year-to-date Bitcoin has surged 45%. The rally was triggered by market participant hopes of strong economic outlook, rapid reversal in US monetary policy, the turmoil in the US banking industry, the SEC approval of eleven physically backed spot Bitcoin ETFs on January 2024 and the fourth Bitcoin halving completed on April 2024. The approval of spot Bitcoin ETFs represents a resounding institutional validation as an asset class.

The Bretton Woods Agreement of 1944 which pegged other currencies to the dollar, established the US dollar as the dominant currency and the foundation of the international monetary system. Although the gold standard was abandoned in 1971, for the past 80 years, the US dollar has remained the most widely held currency for central banks reserves. To date, over 80% of global trade is conducted in US dollars, about 70% of foreign currency debt is denominated in US dollars and it remains the currency of choice for oil, commodities, exchange transactions and international loans. In times of uncertainty and stress, the US dollar is proving to be the world’s safe haven asset and king. However, is important to acknowledge that a new cycle of innovation is shaping the future of finance particularly in the aftermath of the Great Financial Crisis in 2008-2009. Traditional financial institutions are increasingly vulnerable to the rise of newcomers in the financial technology (FinTech), digital assets and decentralized finance (DeFi).

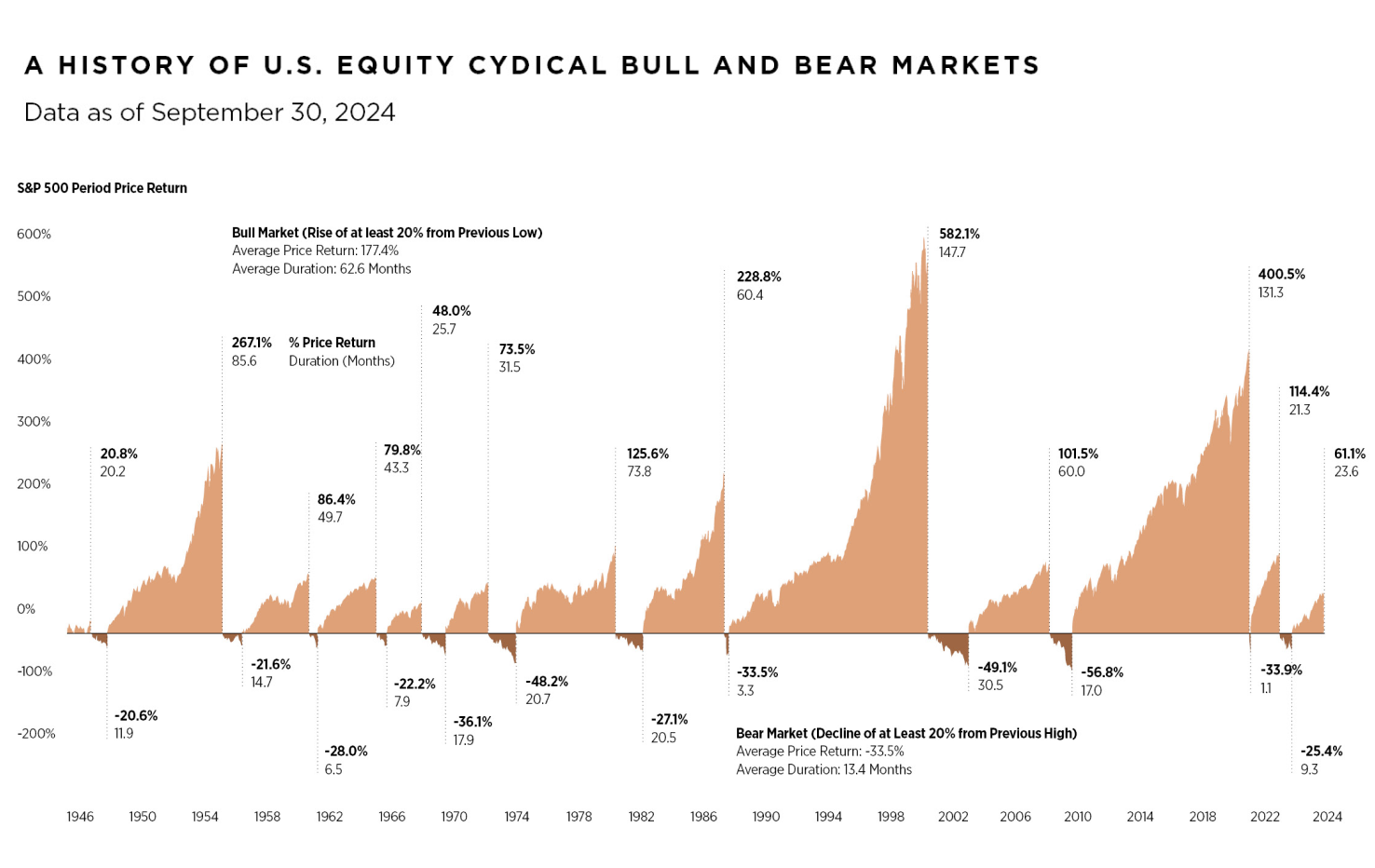

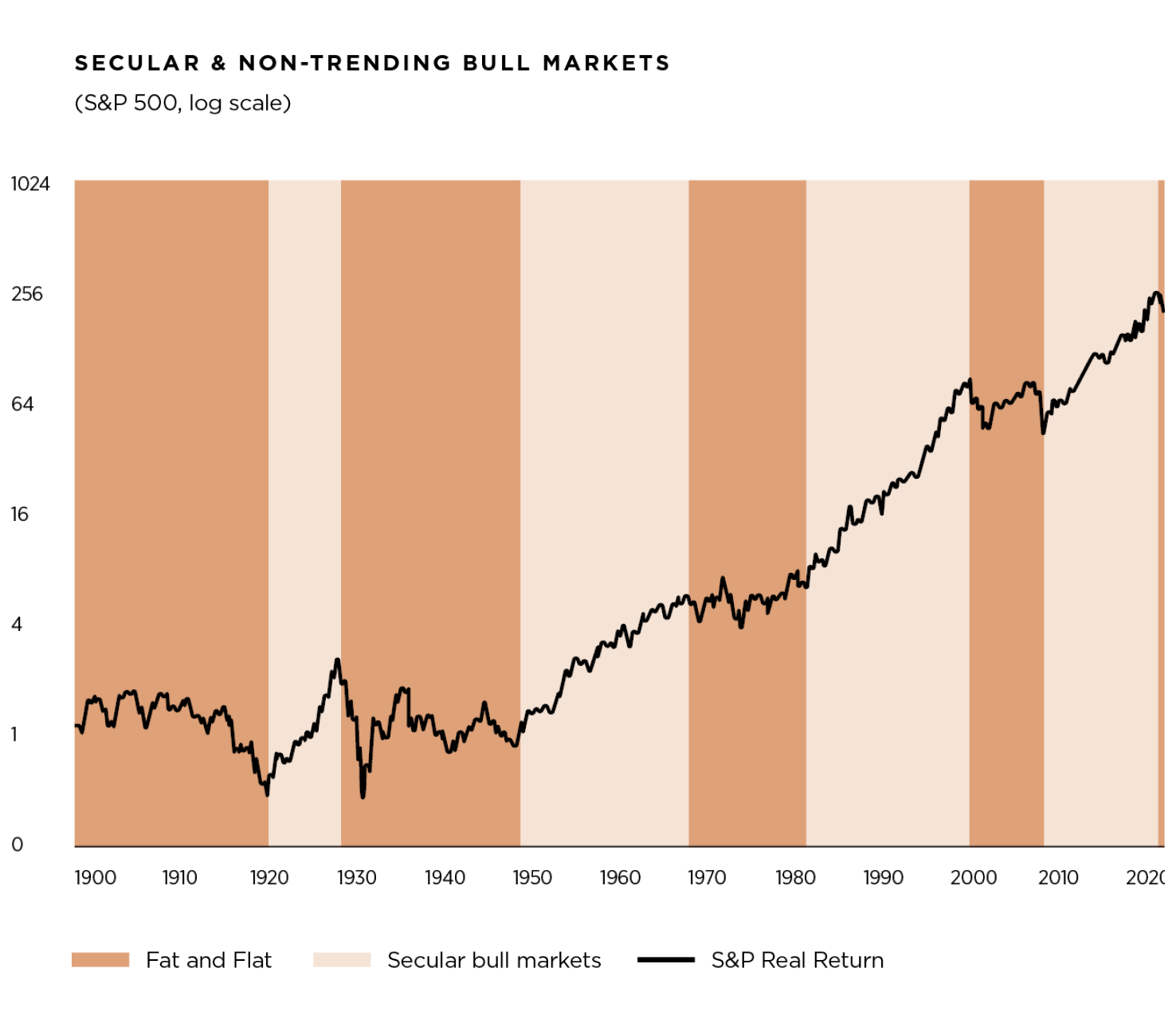

Capital markets are cyclical in nature. Since the late 1920s, the S&P 500 has experienced 29 bear markets and on average bear markets in the US last 26 months. Fortunately, as proven by history, for every bear market, a bull market follows. The start of the bull market almost always begins during recessions when the economy contracts and bad news abound. Since 1946, bull markets last on average 63 months and bear markets 13 months.

While recessions are fairly common, no one knows when the next recession might occur. The US equity market’s domination has accelerated dramatically in recent years particularly since the GFC and have had one of the longest and strongest periods in history of outperformance relative to non-US equities, bonds and cash.

Global money market funds have a record USD $9.5 trillion in assets. Some market participants believe that the current FED easing cycle will likely spur a rotation out of money markets mutual funds into equities. However, from an historical perspective, more than rate cuts, the economic growth environment is the one that determines the faith of equity flows. If the US economy avoids a recession, equity funds typically register inflows whereas if the US economy enters a recession, shortly after the start of the cutting cycle, equity funds generally register outflows.

To maintain its exceptional status and hegemony, the US must continue to serve as a becon of democracy, education, rule of law, economic stability and a leader in the international order. We believe the factors that underpin US preeminence and exceptionalism will continue to persist into the foreseeable future.

Pedro David Martínez

CEO, Regius Magazine.

regiusmagazine.com

Homero Elizondo

Head of Research, Regius Magazine.

regiusmagazine.com