he FIFA World Cup is one of, if not the, most well-known and prestigious sports competitions in the world. Every human-being and every generation on the planet knows what the World Cup is. With many having memories and emotions of the tournament tied to family stories, childhood moments and the eras they grew up in. The highs, the lows, the tears, and the glorious triumphs that bring together people of all ages, communities and societies - and in return, uniting a country on the shared journey of participation… with dreams of glory.

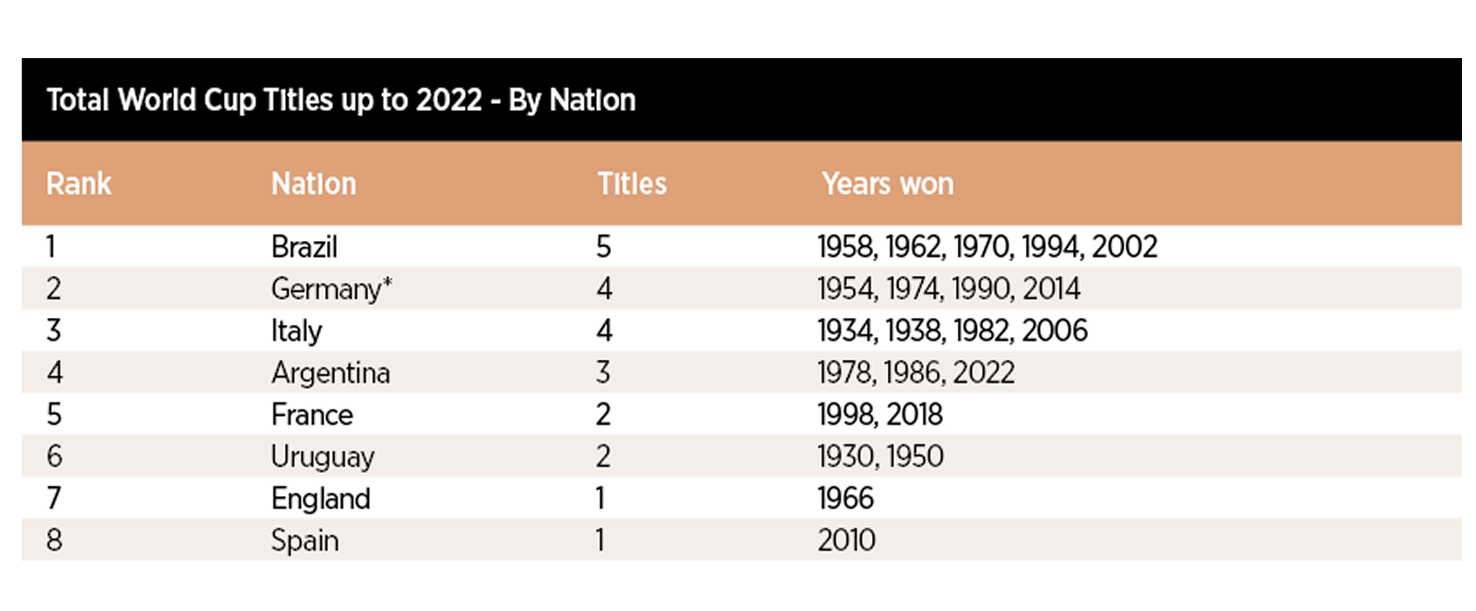

The first World Cup was hosted by Uruguay in 1930. Thirteen teams took part with seven from South America, three from North America and three from Europe. There were no qualifiers, and Uruguay beat Argentina 4–2 in the final to claim the first trophy. Since 1950, the tournament has been held every four years and has grown from 16 to 24, then 32 teams from 1998 to 2022, and now 48 teams for the 2026 edition. The expansion highlights the commercial and societal appeal of the competition and FIFA’s ongoing push for inclusivity.

The 2026 FIFA World Cup is forecasted to become the most watched event in global broadcast history. With 48 countries and three co‑hosts for the first time, being the United States, Mexico and Canada, this 23rd edition epitomises the shift of the World Cup from a single‑nation event to a growing continental platform. Only 2022 was co-hosted with South Korea and Japan. With the 2026 World Cup, US and Mexico will be hosting for the second and third time respectively, and Canada staging the tournament for the first time.

According to official FIFA announcements, there is a projected total ticket inventory of roughly seven million seats across 104 matches. Over 500 million ticket requests were already submitted during the first sales phase with live demand dramatically exceeding in‑stadium supply. Several million more fans are expected to engage through official fanfest activations, while a global television and digital audience is forecast to reach into the billions.

"The 2026 FIFA World Cup is forecasted to become the most watched event in global broadcast history. With 48 countries and three co‑hosts for the first time, being the United States, Mexico and Canada, this 23rd edition epitomises the shift of the World Cup from a single‑nation event to a growing continental platform"

| COMMERCIAL POWER: HOW THE REVENUE MODEL IS EVOLVING

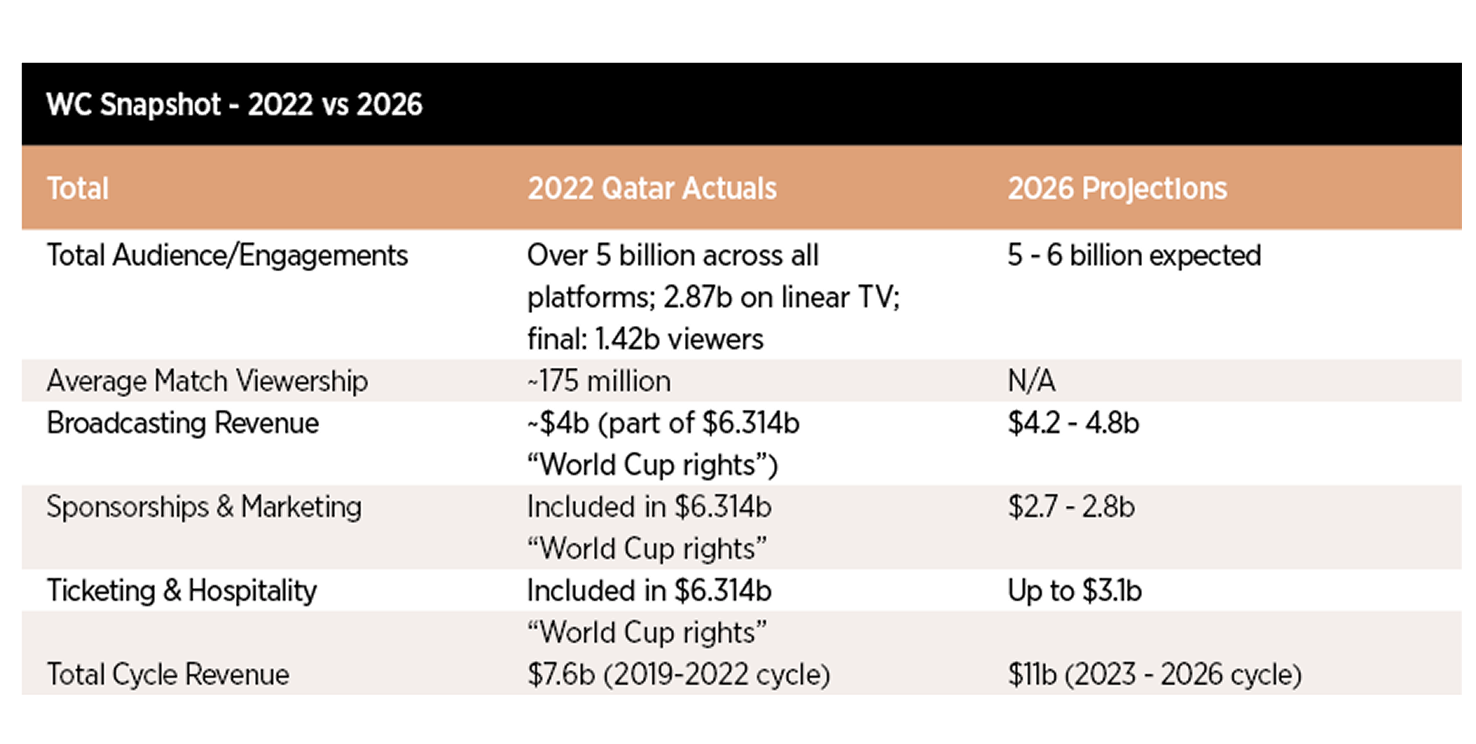

Commercially, the 2026 World Cup revenue model has evolved from Qatar 2022, with key shifts in structure, categorisation and revenue drivers based on FIFA’s official 2023–2026 budget. FIFA now projects more standalone revenue streams rather than bundling everything under “World Cup rights”, reflecting the 48‑team expansion, three co-hosts and in‑house hospitality management:

● Hospitality & Ticketing Rights

Have shifted from outsourced fees to direct sales via On Location (a TKO subsidiary), with projections of up to around $3.1 billion, a major increase on the roughly $0.95 billion that was bundled into 2022’s World Cup rights line. Premium packages, running into high four‑ and five‑figure price points, prioritise corporates and high‑yield consumers.

● Sponsorships & Marketing

Have standalone projections of about $2.7 - 2.8 billion, up strongly on 2022, driven by layered tiers and host‑city activation that unlock a broader local sponsorship economy.

● Broadcasting

Is expected to remain broadly stable in the $4.2 - 4.8 billion range, but with more inventory (104 matches) and time zones favourable to both American and European markets, with a large share already pre‑sold.

● Football Clubs

Benefit with a $355 million fund that will compensate clubs for releasing players. This is now extending to those involved in qualifiers rather than only the final tournament, an increase from $209 million in prior cycles.

The commercial return of the World Cup is clear, especially with the re‑structured revenue model and the tournament being spread over a wider geographic region. But the key question we ask is: what is the impact of the FIFA World Cup beyond the pitch and the media rights?

| BEYOND BROADCAST: LEGACY, INFRASTRUCTURE AND GDP

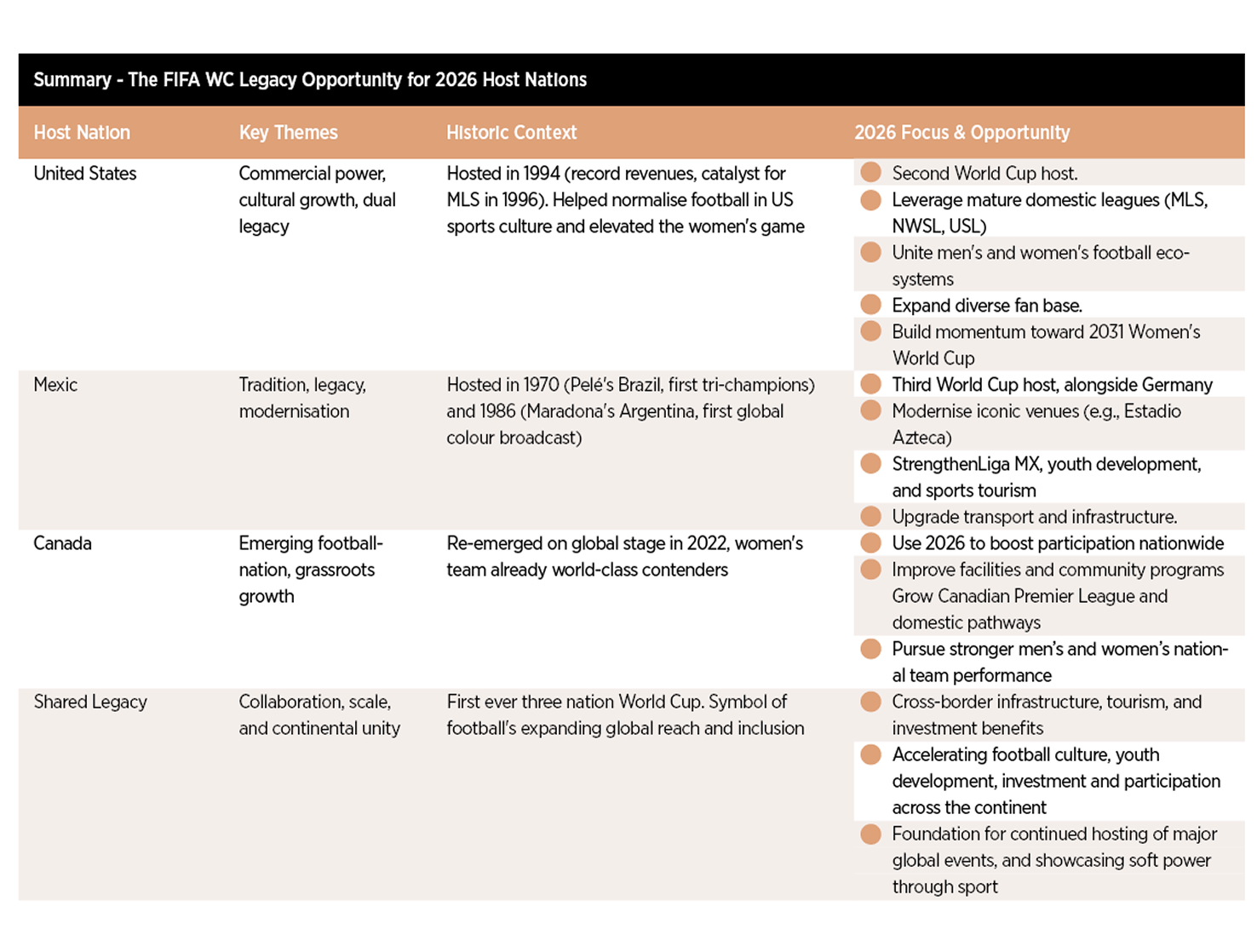

Global mega-events like the World Cup extend way far beyond sport. They showcase host regions to drive tourism, investment and soft power - but outcomes depend entirely on how infrastructure and spending are utilised post-tournament. For reference and purpose of this article, we will use Brazil 2014, Qatar 2022, and the latest 2026 World Cup with US, Mexico and Canada as examples as to how each event is leveraged differently within their unique political and economic contexts.

Brazil 2014: A Cautionary Tale

Brazil was one of the most anticipated World Cups considering it’s reputation in global football. With hope of revolutionising the Brazilian economy, the country spent $13-15 billion on the 2014 World Cup leading to a deflated impact post-event. The country overran early projections by approx. 75%. Stadiums built in low-demand locations became under-utilised "white elephants" and unable to keep maintenance costs. Tourism and GDP forecasts fell way short of expectations, and the tournament drew scrutiny over a host of matters including, inequality, corruption allegations, and underfunding of healthcare and education sectors.

Qatar 2022: State-Driven Transformation

Qatar however is a different story. The State invested approx. $200 billion across stadiums, transport, accommodation and new districts - essentially a blank canvas, which very few host regions are able to do. Unlike Brazil, this was embedded in a long-term national strategy to diversify from gas dependency and showcase Qatar to the world. The metro, airport and road upgrades now serve residents and future events, with several stadiums designed for downsizing or repurposing – and a plan linked to Qatar’s 10-Year Legacy project.

US, Mexico & Canada 2026:

Leveraging Existing Assets

Qatar's strategy for sure doesn't translate to 2026's multi-nation, market-driven format across three mature regions with largely pre-existing stadiums and infrastructure. The real test will be connecting incremental World Cup spending to regional priorities. Success hinges on utilisation and using the ‘short-term’ visibility boost as a platform for more ‘permanent’ growth and leverage, and maintain capital flow. If this plays out well post-event and tied into a wider state / regional strategies, the event has potential to boost impact for future outcomes.

Importantly, and from a US perspective, the 1994 World Cup’s most visible “legacy project” was MLS. There has not been another single initiative of that magnitude since. The cumulative effect of three decades of league growth combined with the impact of 2026 could provide significant value, as:

● MLS club valuations continue to rise, fuelled by media rights, expansion fees and growing attendances, with the growth of MLS NEXT.

● USL being positioned as a genuine development and community platform, adding markets and building its own commercial narrative with real estate anchored commercial opportunities.

Moreover, for Mexico, 2026 will seek to amplify Liga MX - already the world's most-watched domestic league in the US, drawing US investment (Atlas FC sale), deepening MLS ties via Leagues Cup/official matches, and funding club/infrastructure growth. Canada's legacy focuses on participation, facilities and long-term performance over quick financial gains.

| A CHANGING LANDSCAPE: INVESTORS, STRUCTURES AND ATHLETES AS OWNERS

US Investor Appetite and Underlying Assets

Now we have discussed the FIFA World Cup as a global showcase, we will explore the changing landscape inside the business of football. Investor appetite has grown significantly over the last decade.

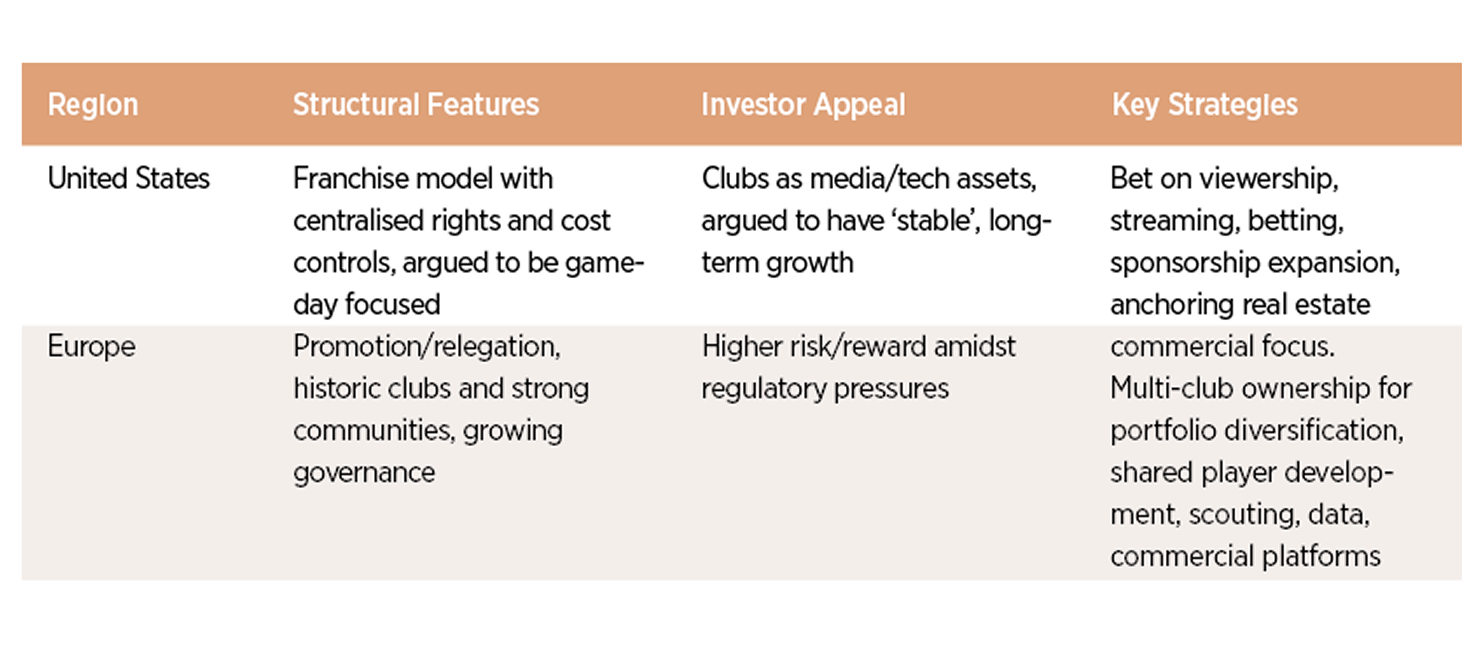

Rising investor appetite over the last decade now sees US investors controlling significant stakes across different regions. As an example, this includes 13 Premier League clubs (e.g., Chelsea, Liverpool, Arsenal, Man Utd), 6 Serie A teams (e.g., AC Milan by RedBird Capital, Genoa by 777 Partners), and also La Liga rights in Spain. Mexico has also gained investment through notable deals with 49% of Club América sold to the General Atlantic/Kraft Group at a $490m valuation, and Querétaro being the first fully US-owned Liga MX club.

The reasons for these acquisitions differ considering the different sporting dynamics between the US and Europe. Many US investors see Europe as ‘undervalued assets’ with the opportunity to inject capital for growth across operations, expanding and multi-purposing retail, real estate and stadium infrastructure, player development models, fan engagement and so on. By taking their differing model and approach in the US, they see opportunity to bring this to Europe. The question remains however, whether they are effective at blending the dynamics.

More importantly, there is a growing recognition that the most resilient returns often sit in the underlying operational assets: training centres, youth academies, data and analytics businesses, IP, women’s teams and communities that can be scaled sustainably. Rather than viewing the World Cup purely as a trigger for valuation spikes at the very top, sophisticated investors are using it as a way to explore the full value chain and allocate capital across multiple layers.

Gone are the days of acquiring a sports team for the sake of sport. We are now looking at sports assets as multi-leveraged platforms across various business interests.

| ATHLETES AS EQUITY HOLDERS – FROM PELÉ TO RONALDO

Historically, legends like Pelé helped globalise the sport through on field brilliance and iconic endorsements. His move to the New York Cosmos in 1975 is widely credited with turning football into a mainstream concept in the US, attracting fans, broadcasters and corporate sponsors, and laying the emotional groundwork that ultimately led to the 1994 World Cup. Pelé’s impact is difficult to measure, but it is deeply woven into the region’s football story.

Today’s athletes are adding a new layer: ownership, and the shift to an investor mindset has accelerated sharply over the past decade. US athletes (and celebrities) are now scouting global opportunities, drawn to Europe’s mega brands and still accessible valuations compared to top US franchises.

For example:

● LeBron James holds a stake in Liverpool FC.

● Tom Brady in Birmingham City FC.

● Kevin Durant in Paris Saint Germain.

● Giannis Antetokounmpo in Chelsea FC.

Furthermore, European-based footballers have never been so active. Recently, Cristiano Ronaldo (CR7) has taken a 25% ownership stake in UD Almería (Spain), leveraging his tremendous brand impact and current portfolio. Other examples include, Gerard Piqué acquiring FC Andorra in 2018 through his company Kosmos, taking the club from Spain’s lower tiers into the professional ranks and into the Segunda División, one step below La Liga. Former Man Utd and France footballer Patrice Evra becoming one of the key investors behind Estrela da Amadora in Portugal, participating in the MYFC fund that bought around 90% of the club’s football company - with an explicit plan to modernise operations and return the team to the top flight.

On the other side of the Atlantic, the game’s most iconic former players have taken ownership stakes in MLS and USL clubs. David Beckham is a co-owner and the public face of Inter Miami, having exercised his MLS expansion option and helped build a franchise now valued at over a billion dollars alongside local partners Jorge and José Mas. Paolo Maldini co founded Miami FC in the NASL era as co owner, fronting the football side of an ownership group that included media executive Riccardo Silva and international investors. More recently, former US footballer, Jozy Altidore (115 US National caps and 42 goals; with NBA star Russell Westbrook) has joined the ownership group of USL franchise Oklahoma City FC.

These cases show that ownership is no longer a retirement vanity project but a serious strategic move where ex players bring their networks, media reach and understanding of dressing room culture into the boardroom.

However, there are two sides of the story. Greatness on the field does not guarantee the same success as ownership. The most prominent example is, the ‘original’ Ronaldo (R9, ‘O Fenômeno’) who was majority owner and President of Real Valladolid in Spain between 2018 – 2025. Despite two promotions, the club also suffered two relegations and intense fan protests, and R9 ultimately agreed to sell his stake after a turbulent tenure. Another example is Spain’s record goal-scorer David Villa as founding owner of Queensboro FC, which was scheduled to join the USL Championship in 2021. The project seems to have faded out with no update on progress. Not every player led project turns into success based on reputation.

Nonetheless, the signals are there. Current and former icons are increasingly seeing club equity and governance as the natural next stage of their careers. It is a logical evolution. These athletes understand culture, fan distribution and commercial leverage better than ever before, and are using that to buy into clubs, launch academies, back sports tech and media ventures, and support women’s football. From high profile stars taking equity positions in US and European based clubs, to ex players moving into leadership roles, there is a clear shift from a wage only mentality to an ownership and influence mindset. With brand equity and their own global distributions, there is plenty of opportunity for these athletes (and celebrities) to elevate the trajectory of the clubs they touch - but as Ronaldo’s Valladolid experience shows, ownership is a high risk, high reward game with few complete outliers (Ryan Reynolds and Wrexham AFC, anyone?).

"Current and former icons are increasingly seeing club equity and governance as the natural next stage of their careers... these athletes understand culture, fan distribution and commercial leverage, and are using that to buy into clubs, launch academies, back sports tech and media ventures, and support women’s football"

| THE RISE OF WOMEN’S FOOTBALL

Other than investment into the game, one of the most powerful growth stories is the rise of women’s football. World Cup audiences, club attendances and media rights for the women’s game are perceived to be increasing, and more investors are now treating women’s properties not just as “add‑ons” to men’s teams but as standalone growth assets with distinct audiences, brands and participation bases.

Recent activity includes the acquisition of FC Badalona’s women’s team in Spain by Mercury/13, adding to portfolio with FC Como Women (Italy). And to prove the seriousness of women’s football, US billionaire investor Michele Kang’s $55 million investment strategy looks to revolutionise women’s sports, focusing on infrastructure and research. She owns a multi-club women’s portfolio including NWSL’s Washington Spirit (US), OL Lyonnes, formerly known as Olympique Lyonnais Féminin (France), and London City Lionesses (UK), and has also committed $30 million towards youth development and coaching.

With women’s sports assets, there are both sides to explore. On the one hand, there is clear potential to leverage existing infrastructure, commercial networks and fan bases to scale women’s football more quickly when it is integrated within a broader club structure. On the other, there is the argument that women’s clubs should be capitalised and governed on their own terms, with purpose‑built brands, products and revenue models, rather than being permanently positioned as secondary to men’s entities.

The most interesting models seem to be hybrid with women’s teams benefitting from shared resources but are valued, marketed and measured as independent businesses. Depending on the context of the asset, it can be debatable as to whether women’s football will maintain its growth towards more mature assets, and how robust this ‘growth’ is. Either way, viewing the asset in its own context and opportunity would be the crucial defining factor for an investor’s desired outcome and ROI.

| CONCLUSION

The US has already benefited from the World Cups it has hosted. Few could have predicted the rise of the sport, especially in the United States from the days of Pelé with the Cosmos, through 1994, to Lionel Messi in MLS today. The 2026 World Cup will not, on its own, guarantee a perfect legacy. But it will act as a powerful catalyst, revealing how prepared federations, leagues, investors, cities and communities are to convert a one‑month spectacle into the next decade of sustainable growth.

For those of us working in and around the game, the World Cup is best understood as a way to showcase visibility and growth potential, globally. Other than the short-term boost, it can accelerate participation, infrastructure and innovation but it can equally accelerate poor governance, over‑leverage and short‑termism if decision‑makers chase the headline rather than the fundamentals.

As for the growing investor appetite and sport being positioned as multi-leveraged platforms, it is hard not to be excited by the capital flowing into football. But caution must be given, especially to those who are entering the game. Rights fees and club valuations have grown in a way that is not always matched by underlying cashflows with many balance sheets leaning heavily on future media, sponsorship and betting revenues. At the same time, fan behaviour is shifting towards shorter, more personalised content, and more regulation is coming in based on club ownership models. Crucially, brand identity and culture differs between regions, and we are seeing growth in newer, emerging sports leagues and properties.

The ones that will be successful in the area of sport, are those who are able to foresee where the sport is going in the context of that asset, the impact of such events, and being able to evolve existing models with tomorrow’s future.

Amrish Vasdev

Founder at Quest22, and Chief Advisor to GrowthStrategy US.

quest22.co

Joe Fraga

Longtime agent, representative, and manager for soccer legend Pelé, as well as a representative for the Pelé Foundation.

pele10.org